This page is not a current Christchurch City Council document. Please read our disclaimer.

![]()

|

|

The aim of this study has been to provide a framework for the assessment of the total cost of waste management in Christchurch, achieved through five objectives:

1. acquire a contextual overview of waste management issues in general and specifically for Christchurch City;

2. identify the components of `total cost' of the Christchurch City Council Draft Waste Management Plan for Solid and Hazardous Waste 1998;

3. identify which components of total cost can be measured and how they may be measured;

4. analyse the potential for measuring component parts of total cost in common units, including money; and

5. recommend how the Christchurch City Council should assess the total cost of its waste management.

The first objective is addressed throughout chapters two and three. Chapter two identified roles of organisations with an interest in NZ waste management, the waste management policy framework and themes in NZ waste management. Chapter three provided further background to total cost assessment, discussing issues including assessment of past and future costs, the difference between private and public delivery of waste management services, effects of waste management on tangata whenua, the relationship between TCA and generator pays, transboundary waste movement, national coordination, measurement in common units, particularly monetary (objective 4), and the nature of effects.

These issues have shaped development of the TCA framework as well as the approach to its implementation and applications. Chapter four develops the TCA framework, drawing on the variety of different options for cost assessment investigated. The framework identifies the programmes of the waste management system (objective 2) and the characteristics of the environment which these programmes affect. Steps of identifying, measuring and calculating costs and benefits are undertaken, guided by criteria which respond to objective 3. Although not the main focus of the study, the framework includes reporting and evaluation as its final two steps.

Having developed the TCA framework and discussed its merits, this chapter considers where CCC should proceed with implementing TCA. This chapter summarises the process of developing the TCA framework and considers whether the framework should be implemented (options). Conclusions are then drawn which bring together key themes through the report, followed by recommendations as to how the framework should be implemented (if implementation is desirable) and priority actions for CCC. The structure for this synthesis is illustrated in figure 8.

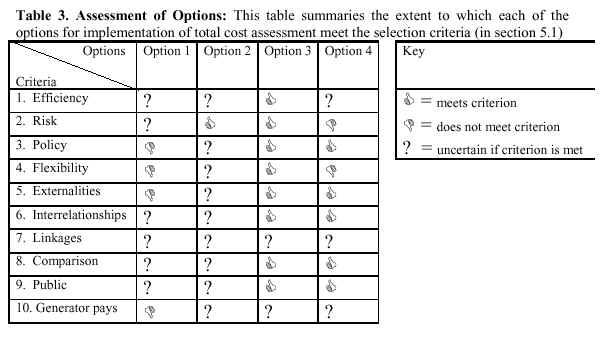

In considering whether to implement total cost assessment, four options for CCC have been identified. The four options are described and evaluated using the criteria specified below. Implications of each option for Christchurch City Council are discussed. These are summarised in table 3. The criteria to assess options for CCC include those specified in section 4.1 to assess the TCA framework and two additional criteria (numbers one and two below).

An option should:

1. enable efficient use of Christchurch City Council resources;

2. not expose Christchurch City Council to an unacceptable level of risk;

3. meet requirements of the Draft Waste Management Plan for Solid and Hazardous Waste 1998 and other policy applicable to Christchurch's waste management;

4. be flexible enough to apply future waste management practices;

5. include social, biophysical and economic "externalities" in the assessment of costs and benefits;

6. enable the inter-relationships between social, biophysical and economic effects to be clearly identified;

7. link causes and effects of waste generation, so that effects (costs and benefits) can be directly traced back to their causes;

8. provide a clear break-down of costs and benefits of waste management practices which will allow the comparison of practices;

9. be transparent, accountable, understandable and feasible so the public can support the process; and

10. be in a format that works towards a system of generator pays charging for waste management services, without precluding other applications.

Option 1: Do not consider TCA as a potential method for meeting waste management and legislative requirements.

Discontinue any investigation of TCA and its potential application to waste management in Christchurch City. Consider and investigate other waste management methods and tools (appendix 2).

Implications:

In ruling out TCA as an option, it is uncertain whether CCC will be pursuing the most efficient method of meeting their waste management requirements and whether this poses any risk to the council (ie. pursuit of other options may entail greater risk). Some national, regional and local waste policies or objectives will not be met (eg., including national waste policy (section 2.2) and principle 4 in the Environment 2010 Strategy). Flexibility is forfeited and all `externalities' will not be included in the assessment of costs and benefits unless some form of TCA is undertaken. It is uncertain whether criteria 6-9 will be met as this will depend on the characteristics or qualities of alternative methods pursued to meet CCC's waste management requirements. This option will not provide a sound basis for generator pays as it is defined in principle 4 of the Environment 2010 Strategy.

Option 2: Do not implement the TCA framework (described in chapter 4). Continue to investigate TCA and other potential methods of meeting waste management requirements and/or wait for further national or regional guidance on total cost assessment and reporting.

Other potential methods for meeting waste management requirements are discussed in section 4.2 of this report.

Implications:

The TCA framework developed in chapter 4 should be judged on its merits, limitations and soundness of rationale used in the selection of options. If the framework is not utilised, then a new approach needs to be developed given the absence of established models or examples of TCA. For this option, further resources are required. This option is relatively risk averse as the information will not be lost through further investigation. Criteria 4-10 may be met for this option but this is uncertain and will depend on the quality of alternative approaches to TCA or other methods pursued. The success of this option may depend in part on whether national or regional guidance for total cost assessment and reporting is likely to be forthcoming.

Option 3: Implement the TCA framework (described in chapter 4) in stages, using a process of continuous improvement and evaluation, and continue to consider other potential methods for meeting waste management requirements.

Implement the TCA framework using one waste management programme as an initial pilot case. Evaluate the usefulness of the framework using the criteria specified above. Continuously improve the TCA framework as further guidance or information is made available and as practical implementation issues are encountered. Continue to evaluate other methods for meeting waste management requirements.

Implications:

This option allows for efficient use of CCC resources given that the TCA framework provides a foundation for developing a system of total cost assessment and reporting. Treating the TCA framework as a `starting point' (for developing a system of total cost assessment and reporting), incrementally implementing and continuously improving the framework using a small-scale approach, enables CCC to better plan resource requirements over time. This increases the council's ability to plan efficiently and minimises risk associated with large-scale implementation (ie. any changes to the framework and associated resource requirements will only be incurred for the pilot case).

All national and regional policy requirements and Principle 4 of the Draft Plan are met for this option. CCC would be able to take a leadership role in total cost assessment, as it would likely be the first Regional, District or City Council to implement a system of total cost assessment and reporting in New Zealand (and possibly further abroad). Requirements to address tangata whenua issues are accommodated within the framework but require further development and input from tangata whenua (section 4.4.1).

This option retains flexibility by continuing to consider other potential methods and by adopting an implementation process based on the principle of continuous improvement. The TCA framework meets criteria 5, 6, 8 and 9 (section 4.5.1). It is uncertain how comprehensively criteria 7 and 10 are met (see discussion above). By adopting option 3, the TCA framework will be of limited availability for potential applications (section 1.2) in the short term. However, this gradual process facilitates greater education and understanding, and enables a smoother transition (from existing accounting and assessment to the TCA framework) and greater `ownership' by staff, private contractors and the public (section 4.4.5). It will be necessary to develop a method for evaluating the performance of the framework and to identify methods/tools for the assessment of specific effects (costs and benefits).

Option 4: Comprehensively implement the TCA framework (described in chapter 4)

Immediately follow each of the steps required to implement the TCA framework (chapter 4) for all of the waste management programmes outlined in figure 7. Develop the framework as quickly as possible within resource constraints.

Implications:

It is uncertain whether this option will provide for efficient use of CCC resources. This follows because of increased risk associated with comprehensive implementation. Given the complexity of and limited existing research on TCA, the risk associated with comprehensive implementation and potential large-scale changes to the framework is considered high. The same advantages of meeting policy requirements and providing leadership as for option 3 are provided. Tangata whenua issues are accommodated within the framework but require further development and input from tangata whenua (section 4.4.3). Some flexibility is retained for this option as the framework is designed to include future changes in waste management practice (section 4.5.1). However, flexibility is limited because CCC will commit to this particular method for meeting waste management requirements and therefore preclude input from other potential methods. Flexibility is also reduced by limiting the council's ability to successfully implement the TCA framework over time. Eliminating the need to investigate other methods for meeting waste management requirements corresponds to a decrease in CCC resource requirements. The TCA framework meets criteria 5, 6, 8 and 9. It is uncertain how comprehensively criteria 7 and 10 are met. Adopting a comprehensive approach to implementation of the TCA framework may enable more rapid use of the framework for the applications described in section 1.2. However, there is a risk (described above) that large-scale changes to the framework and reduced understanding and `ownership' by staff, contractors and the public will limit usefulness for potential applications (eg., if staff or private contractors are unhappy with the new system and will not assess or record costs, then the accuracy of the framework is compromised). It will be necessary to develop a method for evaluating the performance of the framework and to identify methods/tools for the assessment of specific effects (costs and benefits).

The requirement to establish a method for assessing and reporting total cost is made clear in national and regional legislation and policy guidelines, and gives rise to principle 4 in the Draft Plan. Some guidance on the assessment of environmental effects has been provided at a national level, although specific guidance on how to assess and report the total cost of waste has been limited and is not a current priority.

The management of waste is a complex and inter-related process which involves many organisations with direct or indirect responsibility for policy development and/or implementation. Developing a system of total cost assessment for CCC therefore requires a comprehensive, integrated and systematic approach which considers relevant issues and the specific needs of Christchurch City.

Irrespective of the method (ie. TCA or `other' methods) used to address waste management requirements, it is important that waste managers retain a clear focus on long term and fundamental objectives or goals. In developing any type of information system (such as TCA), the objective is to provide a sound basis for waste management decisions. The ultimate goal of these decisions is to establish a system of waste management which will give rise to desirable standards of behaviour (eg., following the international waste hierarchy).

CCC have commissioned this research with a primary interest in the potential application of TCA toward a system of generator-pays charging. This study identifies inherent limitations associated with this application, but recognises that TCA may still provide an imperfect but valid basis for a system of generator pays. The ultimate goal of generator-pays charging is to create the appropriate balance of (market) incentives which give rise to desirable standards of behaviour. A system of generator-pays is only one of several potential TCA applications which include annual reporting, education and promotion campaigns, best management practices and meeting the implementation needs of the RMA.

TCA of waste management is a relatively new field of research which has received little attention internationally. The TCA framework (described in chapter 4 of the report) provides a first step or `starting point' for Christchurch City Council, and is not intended as a complete or prescriptive approach to implementing a system of TCA. Areas for future research have therefore been identified and recommendations are provided. The recommendations relate to the implementation and reporting of total cost assessment.

In deciding whether to implement a system of TCA, having considered the four options and their implications (in terms of the degree to which specified criteria are met), it is clear that option 3 best meets the criteria (as summarised in table 3). Accordingly, our recommendation is to follow option 3, as follows:

Implement the TCA framework in stages, using a process of continuous improvement and evaluation, and continue to consider other potential methods for meeting waste management requirements.

The recommendations in this section provide guidance for how to go about the implementation (option 3) selected above. These recommendations address the issues raised in chapters three and four of the report, and have been evaluated against the criteria specified in box 6, within the respective sections where they are raised as an issue. As illustrated in figure 8, the first set of these recommendations is broken into those relating to coordination, strategic implementation, future costs and benefits, and reporting. The further recommendations relate to application of the framework, further research and the priority actions for CCC.

Out of all recommendations identified above, the following are considered priority actions for CCC.

|