This page is not a current Christchurch City Council document. Please read our disclaimer.

![]()

|

|

The third chapter discussed issues which influence the way in which total cost assessment should be carried out. Chapter 4 introduces a framework within which TCA can be carried out. A framework is necessary to provide a systematic approach to deal with the broad and complex range of information encompassed by `total cost'. A framework can minimise inconsistencies in carrying out TCA, such as missing out or double counting costs and benefits. It can also incorporate other approaches such as the national State of the Environment Indicators Programme (MfE, 1997c) or current monitoring activities. A framework enables costs and benefits to be compared between CCC and other waste management organisations. In addition, a framework provides a means for integrating social, biophysical and economic aspects, enabling thus recognition of their interrelatedness. Integration of social with biophysical matters is of particular concern to CCC (LGNZ, 1998).

Chapter 4 provides criteria which a TCA framework should meet. Existing approaches to cost assessment are outlined, their usefulness discussed, and the approach taken using the framework presented in this report is outlined. Section 4.4 introduces this framework and discusses each of its steps:

1) identifying waste management programmes;

2) identifying activities and sub-activities of each programme;

3) identifying the characteristics of the environment;

4) identifying potential effects of specific activities;

5) measuring the magnitude of effects;

6) calculating effects in units of cost and benefit;

7) compiling the total cost table;

8) reporting the total cost of waste management; and

9) evaluation of the framework.

These steps are illustrated in figure 6.

Box 5 specifies criteria for a framework for TCA, which have been developed to assess the various options for developing a TCA framework. These criteria are not listed in order of priority. The rationale for each criterion is provided below.

Box 5: Criteria for a framework for total cost assessment.

A Total Cost Assessment Framework should:

1. meet requirements of the Draft Waste Management Plan for Solid and Hazardous Waste 1998 and other policy applicable to Christchurch's waste management;

2. be flexible enough to encorporate future waste management practices;

3. include social, biophysical and economic "externalities" in the assessment of costs and benefits;

4. enable the inter-relationships between social, biophysical and economic effects to be clearly identified;

5. link causes and effects of waste generation, such that effects (costs and benefits) can be directly traced back to their causes;

6. provide a clear break-down of costs and benefits of waste management practices which will allow for comparison of practices;

7. be transparent, accountable, understandable and feasible so the public can support the process; and

8. be in a format that works towards a system of generator pays charging for waste management services, without precluding other applications.

The following discusses the rationale for selecting each of the established criteria:

1. It is the aim of this report to provide a TCA framework which can be implemented by the Waste Management Unit of the CCC. Thus, the framework must be consistent with the forthcoming CCC Waste Management Plan. Also, the framework should regard legislative requirements such as the RMA and the LGA, policies such as the Environment 2010 Strategy (MfE, 1995) and the Regional Policy Statement, and international agreements which influence waste management.

2. Waste management practices can change relatively quickly over time, for example, due to changes in policies, market prices or social and ecological circumstances. It is recognised, for instance, that there may be significant changes to the Draft Plan before its final release. Planning and implementing a framework for TCA is a complex process which requires a long term approach. A TCA framework must therefore be sufficiently flexible to incorporate changing waste management practices.

3. The Draft Plan states that the "real costs of waste management shall include social, environmental and economic costs...". Social and biophysical costs and benefits are often underestimated or disregarded in current economic assessments, particularly in waste management (Turner, 1995; Hirshfeld et al., 1992). Considering a limited range of costs and benefits distorts decision making and the inclusion of current `externalities' will lead to integrated policy making, addressing overall well-being.

4. The inter-relatedness between social, biophysical and economic effects is explained in section 3.1. For example, the introduction of pollutants to a stream can cause social, biophysical and economic effects. In accordance with IEM (section 1.3), not only the integration of social, biophysical and economic factors but also addressing their inter-relationships within a framework is essential for sound environmental management. Clarifying the inter-relationships between waste management variables enables their effects be identified and for double counting to be minimised.

5. The link between cause and effect provides valuable information for policy making. If the effects (eg., offensive odour) of an action (eg., turning compost) are clear, management practices or policies relating to them can be revised (eg., alter time of turning compost heaps). This framework criteria reflects the structure of the RMA, which is based on the identification of effects and linking them to activities; a main purpose of the Act is "avoiding, remedying, or mitigating any adverse effects of activities on the environment" (section 5(2)(c)).

6. In order to carry out TCA, the costs and benefits of waste management must be broken down into manageable categories. The selection of the categories enable useful comparison within CCC's waste management system (to guide waste management decisions, eg., Identifying particular aspects with very high costs or benefits) and between CCC's and other waste management systems (to allow for coordination with other local waste management systems in the future if desired).

7. Transparency, accountability, understanding and feasibility are necessary to provide a sound foundation for the assessment of total cost, especially because TCA is a long-term and complex process. This is reinforced by the LGA which requires accounting systems which are generally accepted, and non-financial reporting to facilitate public understanding (section 2.2.7). Also, the CCC Draft Waste Management Plan states transparency together with openness and accountability as its third principle.

8. As outlined in section 1.2, a TCA framework has several potential applications, however charging is a particular focus identified by the CCC, reflecting Government waste policy (MfE, 1992) and regional waste policy (CRC, 1995).

A variety of approaches and tools currently available for cost assessment were considered in the design of the total cost assessment process. These approaches and tools were derived from multiple sources, including national legislation, international organisations, academia and the commercial sector. The following provides an overview of the approaches and tools, and the contribution they may be able to make to TCA. A more detailed description of each of the approaches and tools is provided in appendix 2. Subsequently, the rationale for and process of developing another approach (ie. the framework described in chapter 4) is given.

Approaches provide an overall structure while the tools prescribe a particular assessment method. In practice, they are not used in isolation from each other. For instance, Social Impact Assessment (SIA) could well draw in information gathered by physical measurement methods and information collected in Environmental Impact Assessment (EIA).

Approaches that include quantitative data, but also rely on qualitative description of effects are commonly used for biophysical and social assessment. An example is Environmental Impact Assessment (EIA) which requires, but does not particularly prescribe, tools for assessing biophysical effects. The Fourth Schedule to the Resource Management Act 1991 describes the procedure for the Assessment of Environmental Effects (AEE) which is an equivalent to EIA, designed to comprehensively assess biophysical and social effects. However, no standard form of data presentation is established and effects are often measured in a variety of forms, so that comparisons between effects are difficult to make. Presenting information in a descriptive format limits its potential application, as descriptions are difficult to compare directly. The potential benefit of descriptive or mixed format system lies in the comprehensiveness of the information gathered. In this way, AEE and EIA are valuable in suggesting overall comprehensive approaches to total cost assessment.

EIA can also include Social Impact Assessment (SIA). Both approaches provide an overall structure or approach to cost and benefit assessment. There are a considerable range of tools utilised within SIA and EIA. SIA generally draws on a range of information, utilising existing data such as census figures, physical data being collected, and specialised techniques (for example, consultation or survey methods) to build up a picture of effects. In contrast to EIA, SIA is only concerned with the assessment of social effects, not biophysical effects. Both EIA and SIA can include the assessment of socio-economic effects but are not generally concerned with the financial effects for the organisations involved. Like EIA, SIA is valuable for TCA as an overall approach, used in combination with other approaches and tools.

Life Cycle Assessment (LCA) is also a predominantly qualitative approach, and the same issues relating to `comparability of effects' and the `variety of potential assessment tools within the approach' apply. As with SIA and EIA, LCA is not prescriptive of the specific assessment tools to be used. LCA is a `cradle to grave' approach to assessment. Products are assessed for their effects at every stage of their "life cycle"; from the research and development of the product, through obtaining the raw materials for the manufacturing process, transportation and utilisation of the product, to its eventual disposal. This approach is a current focus of the Ministry for the Environment (S. Baird, pers. comm., 1998). Although this approach is very valuable, the scope of this study has is assess the effects of waste and waste management on Christchurch residents. As many products consumed in Christchurch are imported from elsewhere, and many others are exported out of Christchurch, a LCA approach would involve determining the effects of these. This is not inkeeping with the criteria which guide establishing a the TCA framework, and is well beyond the scope of this report.

Emergy is a system for measuring the costs and benefits of the whole economy (including the use of natural resources beyond the price paid), excluding social effects. "Emergy is the available energy of one kind of previously used up directly and indirectly to make a service or product. Its unit is the emjoule" (Odum, 1996, p.7). Apart from the exclusion of social and future effects, emergy could be a useful approach to TCA because of its comprehensive nature while also measuring effects in one single unit. However, its very complex and technical approach does not provide the transparency and understanding required to meet the seventh criteria of a framework for TCA, and may be beyond CCC's resources.

There are a range of accepted techniques for physical measurements such as air and water quality, or noise and odour levels. Because of the number of highly specific tools, these are not covered in appendix 2, but widely accepted tools should be used and carefully adhered to (eg., see CCC (1997) for water and soil sampling protocols and procedures being used for landfill monitoring). Use of physical measurements as single tools without an overall framework would not address the inter-relatedness between factors, or the link between cause and effect. Measuring the costs of waste in in many different units would limit the application of a TCA framework for developing a systeom of charging. The scientific knowledge required to understand the meaning and implications of physical measurements would also diminish transparency to the public.

Given the breadth of physical measurements and the complexity of biophysical and social systems, the use of indicators of environmental quality is considered potentially useful. An indicator is a measurement used to represent a much larger set of characteristics or system of the environment. The chief use of indicators is to compare environmental quality on large scales and/or over long periods of time with low monitoring costs. Appropriate indicators are very hard to discover, but do result in very efficient monitoring of environmental quality. However, without additional procedures, an indicators-based approach does not associate management decisions (causes) and effects. Using indicators also requires additional conversion for comparison and use in setting charges. So, while useful, indicators require the support of other approaches to fulfil the criteria.

Many assessment and management methods have been developed to use monetary values to aid in decision making. NMV tools attempt to include effects not previously accounted for through the market in a monetary unit. They can also utilise information provided through other tools such as physical measurements. NMV tools can only identify the costs and benefits of biophysical and social effects in an indirect way, ie. by finding out people's willingness to pay for benefits or willingness to accept costs, or by finding comparable substitute markets. NMV tools can not always be applied and can have various biases, as described in appendix 2. They do not necessarily identify the inter-relationships between social, biophysical and economic effects.

Cost-benefit analysis uses the monetary gains (benefits) and losses (costs) associated with courses of action to decide whether to proceed, and to choose between options. CBA is designed to help broaden and improve organisations' financial accounting systems. The approach depends heavily on NMV to assess effects not covered by market transactions. If monetary values cannot be identified appropriately (eg., through NMV), CBA cannot be applied. This is likely to be the case in some areas of waste management, as discussed in section 3.5.

CBAs usually consider the costs of a development or project over its entire life, and convert them to present day terms using discounting (discussed in section 3.8). CBA, SIA and EIA can all incorporate Risk Assessment, the tool dealing specifically with future costs and benefits, and it can be applied to any type of effect. Its outcome can be monetised quantification of risk, but need not be and can be purely qualitative. Risk Assessment is useful to TCA but must be used in conjunction with tools which assess present costs and benefits.

Total cost management (TCM) and Full Cost Assessment use monetary gains and losses to make decisions on processes within a business. They present an overall approach to assessment, and are more prescriptive of the methods within it than for instance EIA. Both TCM and FCA focus on improving accounting systems, TCM as a tool to continuously improve operations, and FCA to increase the consideration of environmental costs. Although FCA is expanding to including externalities, this application is still in its early stages. Thus, TCM and FCA do not usually not meet the third criteria of including social, biophysical and economic externalities.

The preceeding discussion demonstrates that no single approach or tool can encompass everything required for a total cost assessment framework. Every approach or tool requires other approaches or tools to be feasible and useful. Although none of the existing options that were discovered fulfilled all the criteria, many options contributed to the final output. There is overlap and interconnections between the use of many of them, suggesting a combination is feasible. Thus, the decision was made to develop a new approach, incorporating elements of the existing approaches and tools. Various methods of measurement would be placed in an integrated framework, enabling effects to be identified, assessed, and, potentially, compared directly.

Waste management and associated effects on the environment are part of a complex system. Any assessment of total cost will necessarily involve some level of abstraction to reduce the complexity of this system to an understandable set of data. The challenge of designing a process for assessment is to produce a set of data that accurately represents the actual situation while presenting it in a form that allows it to be used in decision-making. The first step of the framework design process was set out in the terms of reference - the development of a categorisation system for costs.

Initially, three main options for a framework were apparent - TCA by effect, by management practice (waste management programmes or activities) and by waste type. Categorisation by effect fits well with the RMA environment and is logical because cost is essentially a way of defining an effect, however there is a need to link the effects back to their causes for this to be useful. Categorisation by waste type is useful because it relates costs of waste to generation behaviour, but it does not make the effects of specific management practices clear. Management activities alone would make the cost of the different management practices clear but not necessarily make the types of effect explicit.

A combination of categorisation methods is necessary. Categorising by both activity and type seemed problematic to the research group. This is because they entail two influencing variables, it would be difficult to see which is the cause. The effects of different types of waste within management activities are also likely to be inseparable in many cases. Categorising by effect and type would face the same challenges of inseparability of effects, and does not lead to accountability of management practices themselves. The option which seemed to best meet the criteria was therefore categorisation by effects and by activity. This would allow accountability of specific management practices, clearly identifying their effects. Because monitoring of the waste stream's composition already occurs in Christchurch on a biannual basis, there seemed to be potential for waste type analysis to be kept as a separate but complementary system.

The total cost assessment process provided therefore involves the definition of activities grouped into waste management programmes within the Christchurch waste management process, and determining the effects that each activity has on each of the different characteristics of the environment. An affecting agent (activity)/affected characteristic (environment) matrix format is used throughout the process for recording the identification and measurement of effects. The matrix is integral to the comprehensive identification of effects, as the presence of the full list of biophysical, social and economic characteristics of the environment forces consideration of all the effects a waste management programme might have, while providing a basis both for systematically working through, and for summarising, the different effects.

Just as the wide range of types of cost encompassed by `total cost' requires a composite framework drawing on a range of approaches, the diversity and complexity means that there are several levels of assessment required for some costs to be evaluated. The total cost assessment framework developed therefore focuses on firstly the identification of effects, then their measurement, then their calculation, and finally their summary and reporting. The framework as a whole is illustrated in figure 6.

Elements in the design of the framework ensure that the results of an assessment will meet the criteria for total cost assessment (box 5). The framework is comprehensive in the identification of effects, ensuring that all effects on biophysical, social and economic characteristics of the environment are identified. This is vital for the inclusion of externalities in the assessment and is achieved through examining each waste management programme for any effects it may have on a comprehensive list of characteristics of the environment. Using activity-based assessment also improves the performance of the framework relative to flexibility, applicability and accountability criteria. The flexibility of the framework is high, as the assessment process directly incorporates the changes in management. Costs and benefits can be directly attributed to waste management decisions, so the total cost assessment data creates incentives for changing behaviour on a large scale, such as how to manage the landfill, and whether to use landfill disposal. The link between the activities and their costs and benefits also allows effects to be traced back to the decision within the waste management process that caused them, creating accountability.

Once identified, effects are examined individually at each stage of the framework. This is important for several reasons. An effect may not be appropriate, feasible and efficient to measure, and that effect will be identified, but not measured. Different effects may require different measurement tools, and may need to be considered separately. Additionally, the sensitivity of the environment may vary from place to place, and similar activities in different locations may have different magnitudes of effects. Effects must also be kept separate where possible to ensure that the links between activity and effect are maintained.

After measurement, the magnitudes of effects will be in many different formats. To enable direct comparisons between activities, some effects can be converted into common units. As discussed in section 3.5, effects cannot be converted into common units unless it is appropriate, feasible and efficient. The framework allows decisions to be made for each effect, based on those three criteria, on whether to convert a measurement into a common unit. Multiple types of units can be used in the framework, so as not to exclude large amounts of information which do not convert to a single unit.

The section above describes the framework for total cost assessment as a whole and has given an explanation of why we have chosen this form of framework. What follows is a more detailed description and discussion of the different steps within the framework. There are nine main steps:

1) identifying waste management programmes;

2) identifying activities and sub-activities of each programme;

3) identifying the characteristics of the environment;

4) identifying potential effects of specific activities;

5) measuring the magnitude of effects;

6) calculating effects in units of cost and benefit;

7) compiling the total cost table;

8) reporting the total cost of waste management; and

9) evaluation of the framework.

In the following sections we discuss the steps outlined above. Figure 6 gives an overview of the framework and the steps and decisions that need to be taken in the framework.

In order to demonstrate how to implement the total cost assessment framework outlined in this report, we have chosen the landfill programme (table 1) as an example. This choice follows the predominant attention landfill programmes have received in literature, especially the attention MfE has given to landfills, including a guide for full-cost accounting (MfE, 1997). The single goal of the Draft Plan also relates directly to landfilling, indicating the importance of the programme in Christchurch (appendix 5).

To provide for a systematic and understandable approach to assessment and reporting of effects and (in keeping with the criteria specified box 5), it is necessary that effects are separated into a series of categories. This means that we need a hierarchical system of categorisation. Costs associated with waste management are many, inter-related and frequently complex. In the absence of a systematic approach it would be unlikely that accounting of total costs would be efficient, understandable or would provide the required/desired information.

Our primary classification of the Christchurch waste management process is by programmes. A description of the waste management process and the programmes is given in section 4.4 and is represented in figure 5.

We have chosen a programme- and activity-based categorisation for the following main reasons:

Assessing total cost in terms of programmes and their associated activities provides for a clear understanding of `cost dynamics'. Costs and benefits are accounted for in terms of the activities which give rise to them. It therefore enables clear identification of causes (activities) and effects. `Activity-based costing' is one of the three main principles of Total Cost Management (Ostrenga et al., 1992, p.30), and is also recognised as a way of providing some degree of Full Cost Accounting information (Willis, 1997). The links between causes and effects also enables CCC to target specific areas (eg., activities with high costs to minimise effects and waste), since effects cannot be managed themselves, only the activities which cause the effects can be managed. A clear definition of the boundaries of programmes is crucial for a transparent, accountable and understandable assessment of total costs of waste management (criteria 7 in box 5). This is discussed below.

To ensure that effects are not forgotten or identified twice within the framework, it is necessary to clearly identify the boundaries for each waste management programme. This section proposes boundaries that can be applied to all waste management programmes, and expands on the information given in section 2.4.4 and figure 5.

There are a number of valid approaches to defining programme boundaries such as the scale, and temporal, operational and policy considerations.

The `scale' of classification is arbitrary. For example, individual past disposal sites might be classified as separate `programmes' as opposed to broadly grouping all of these in the single programme, `Past disposal sites'. For the purpose of developing a TCA framework for this study we have used a broad system of classification. The rationale for this follows that broad definitions are more conducive to understanding by the general public and are therefore more accountable and transparent. This also allows the costs and benefits associated with a given type of waste management programme to be evaluated and compared (ie. toward best and efficient management practices).

Another approach to defining programme boundaries relates to when the management practice occurs in time (ie. temporal separation). For example, landfill could be separately defined as `past', `present' and `future' landfill programmes or be grouped together in some way. For the purpose of developing a TCA framework for this study, we have separated `past' landfill sites from `present-future' landfill sites. This is an arbitrary distinction, but is justified on the basis that the management of past landfill sites (including contaminated sites) and the present (Burwood) and future landfill sites is currently separate.

Grouping present and future landfills as a single programme is advised to ensure that the future effects of using landfill space today can be converted to current costs and benefits. In addition, the costs associated with a future landfill (eg., site availability and set-up costs) may affect the dynamics of cost associated with current management of the Burwood landfill. For example, if future landfill costs are extremely high, investing in waste separation and education programmes (to reduce the use of current landfill space) may be a more appropriate use of resources. For these reasons present and future landfill sites are included in a single programme (section 3.8).

There are a number of activities which do not clearly fit into a specific programme. For example, transportation from a refuse station to the landfill might be included within either of these programmes. This study defines programmes within the TCA framework as including all costs associated with transport to the site where the programme is located (except where it is specifically defined as a separate programme, eg., municipal collection). Including transport in this way reflects the effects that changes in programmes can have on associated transportation. For example, there is a direct relationship between a reduction in the amount of waste disposed at the landfill and the costs of transportation.

There are a number of activities that are universal to all waste management programmes (eg., national policy and planning, general waste management education) or for which some associated costs are universal and some are specific to a programme (eg., on-site landfill administration, recycling education and research). Examples of these activities include administration, research, national policy development and planning, local policy development and planning, education, promotion, and monitoring and enforcement. Where such an activity can be specifically related to an individual programme, the associated cost is directly attributed to that programme. Where activities are universal, the associated costs must be assessed for the activity as a whole, and be subsequently allocated to specific programmes (according to an estimated proportion of resources used).

The international waste hierarchy (box 3) is a tool used by waste managers to prioritise steps in the waste management process and is the focus of NZ Government policy (section 2.3.2). In order to facilitate Christchurch City Council's ability to use the international waste hierarchy as a policy tool, programmes within the Christchurch waste management process (figure 5) have be aligned within categories of the international waste hierarchy.

An issue associated with programme classification is that some of the costs or benefits that relate to a given programme may not be included within the boundaries of that programme. For example, extension of the Recycle and Reuse Programme will divert wastes from other programmes. This will cause in a reduction in the volume of waste disposed at landfill, resulting in a reduction in total landfill costs, and may increase marginal financial costs ($/tonne). Where this is the case, the link between `causes and effects' (and associated costs and benefits) for a specific waste management programme (criteria 5 in box 5) can only be inferred rather than directly calculated.

For each programme, activities and sub-activities have to be defined. These are recorded within the framework in a hierarchical structure which allows all of the activities associated with a programme to be logically accessed. We propose a list of activities and sub-activities for the example of the programme `landfill' (table 1). Information for these divisions have been derived from the Landfill Full Costing Guideline (MfE, 1996a), the Landfill Management Plan for the Burwood landfill (CCC, 1993), 1998/1999 budget notes and calculations provided by CCC, and from proposed accounting recommendations developed by the Canadian Institute of Chartered Accountants (CICA, 1997).

The landfill programme is divided into the main activities `management and administration', `planning', `construction', `operation', `closure', and `after-care'. Each of those activities is then divided into sub-activities. For example, the activity `construction' (3) is subsequently divided into 14 sub-activities, including items such as roads (3.2), earthworks (3.6) and security facilities (3.15). The number of sub-activities and number of levels depend on the degree of detail required. For example, we have included `employment' as a sub-activity in each of the activities rather then pooling it in the `management and administration' activity to provide for more accurate information.

We have included the sub-activity `existing landfill' in the two activities `operation' and `after-care'. This is because effects of disposed waste cannot be directly allocated to a specific activity, however they do have effects on the environment long after they have been disposed of, for example, the affect of leachate on waterways. The sub-activity `existing landfill' provides for the appropriate allocation of those effects.

An example of a division of the activities for one programme is provided in table 1. This might have to be further adapted to the specific needs of the Christchurch Waste Management Unit. In addition, CCC will have to identify the activities and sub-activities for all of the other programmes in the waste management process.

As discussed in section 1.2, the environment is a complex, broad, inter-related and potentially all-encompassing phenomena. B�hrs & Bartlett (1993, p.9) note that human activities which affect one aspect of the environment (eg., pollution of air through waste incineration) may have repercussions in many other aspects (such as forests, waterways, soil fertility and human health and safety). Any breakdown of the environment into categories is therefore arbitrary as overlap between categories is inevitable. In selecting forms of categorisation the aim has been to minimise overlap and double counting of costs in addition to meeting the criteria (box 5). For each category identified, boundaries are distinguished in order to clarify where a given effect should be recorded, as described below.

Characteristics of the environment are broadly classified into `biophysical', `social' and `economic' categories (appendix 6). Definitions for each of these terms are given in section 2.5 and the boundaries of each set of characteristics are clarified below.

1. Biophysical includes all effects on living things (excluding effects on people), the physical environment (including physical processes), and any interactions between them (this is a liberal definition of `biophysical' which includes ecological processes and the intrinsic value of ecosystems).

2. Social includes all effects on society (human populations) and human structures that are not economic effects (see below), independent of whether they are secondary or multiple effects of biophysical effects.

3. Economic includes all effects which are expressed in market systems. Thus, economic effects can be directly translated in financial costs, expressed as a dollar value. Effects which are economic include effects on Christchurch City Council in the delivery of waste management, and socio-economic effects.

These three categories are consistent with divisions used in the Environment 2010 Strategy (MfE, 1995), State of New Zealand's Environment Report (MfE, 1997b) and the Environmental Performance Indicators: Proposals for air, fresh water and land (MfE, 1997c).

The landfill example (table 1) illustrates how each of these broad classifications may be broken down further into sub-categories.

The biophysical category is sub-classified under four headings, (1) land, (2) water, (3) air and (4) atmosphere, as illustrated in table 1. Broad environmental `media' were selected as a method of sub-classification because these are commonly understood and compatible with existing branches of science. For example, geology and edaphic studies relate to the scientific study of land or soil processes, marine science and hydrology relate to the study of the aquatic environment, and biology and ecology are concerned, in part, with the study of biodiversity. The four sub-classifications correspond to the classifications used in part 2 of The State of New Zealand's Environment Report (MfE, 1997b) which describe the state of New Zealand's environment. The proposed Environmental Performance Indicators are closely related to the 11 priority issues for the biophysical environment in the Environment 2010 Strategy (MfE, 1995, see appendix 7). The TCA framework classification system has been established to ensure that the proposed indicators will clearly correspond to framework sub-categories. A reason for this approach, in keeping with the environmental performance indicators programme, is that "standard classification systems...are essential if we want to make meaningful comparisons of indicators within and between different regions" (MfE, 1997c, p.18). This approach will also allow CCC to easily incorporate indicators into the total cost assessment process, if desired.

The category, `Water', is sub-classified under the headings: (i) surface water, (ii) ground-water, (iii) coastal and estuarine and (iv) marine. These divisions recognise the unique nature of the different aquatic media, and correspond to the classifications used in the State of New Zealand's Environment Report (MfE, 1997b).

Each of the water sub-classifications and the `land' and `air' categories are further sub-classified under the headings (i) living, (ii) non-living and (iii) physical and ecological processes. These are defined as follows:

(i) living (biota) includes all non-human living organisms (plants, animals and other organisms);

(ii) non-living (abiota) includes all components of the biophysical environment which are not living;

(iii) physical and ecological processes include all of the cycles and inter-relationships between inorganic (not containing carbon) components of the environment and all of the interactions that determine the distribution, abundance and characteristics of organisms (Chapman & Reiss, 1992).

A process will include either just non-living components, or both non-living and biotic components of the environment. For example, the physical process of erosion only includes non-living components of the environment (ie. water and soil) and nutrient cycles include both (ie. water, nutrients and organisms). This gives rise to potential overlap and double counting of costs. To avoid this we make the following distinction: for a given process the cost associated with effects on the process is recorded under sub-category (iii) (eg., for nutrient cycles the cost reflects the importance of the process on the integrity, form, functioning and resilience of the system), the cost associated with effects on biota and the costs associated with effects on the non-living components of the environment (eg., water and nutrients). In this way the intrinsic values of ecosystems are included within these sub-categories, to avoid double counting. Intrinsic values must be assessed to meet the implementation needs of the RMA and section 1 states that intrinsic values:

in relation to ecosystems, means those aspects of ecosystems and their constituent parts which have value in their own right, including-

a) Their biological and genetic diversity

b) The essential characteristics that determine an ecosystem's integrity, form, functioning, and resilience

The `social' category is sub-classified into the following: (1) health and safety, (2) spiritual, (3) cultural, (4) historical, (5) scientific, (6) aesthetic, (7) land use, (8) recreation and (9) other characteristics. This system of classification is partly derived from those social effects described in the Fourth Schedule (Assessment of Effects on the Environment) to the RMA. The list of social effects in (s2)(d) of the Fourth Schedule is comprehensive, but lacks detail. For this reason, three categories have been added (health and safety, land use and recreation). Effects on tangata whenua have not been specifically included at this stage. Before this is done, consultation needs to be carried out regarding appropriate approaches to assessing and reporting effects on tangata whenua.

Economic characteristics of the environment are classified into three main divisions, the `socio-economic', `directs costs' and `indirect costs' categories. For further discussion of this division see section 2.5 (terminology). Financial effects are included in an accounting system, and sub-categories are developed by the accounting system used.

The matrix as part of the total cost framework shown in figure 6 and in the landfill example (table 1) has been developed so that potential effects of activities/sub-activities on characteristics of the environment can be identified. This has to be done separately for each activity/sub-activity. The first step is to identify whether there is a potential effect or not (presence/absence). If a potential effect is identified it has to be described in the appropriate box in the matrix.

For example, employment has a financial effect in that CCC has to pay salaries and wages. Since these effects have already been translated into financial costs and are accounted for in the current accounting system, they can directly enter the table as a dollar value. Leachate of the existing landfill as another example might have a potential effect on ground water. This effect, if identified, is not accounted for in the current accounting system, and has to be described in the appropriate box[3].

Some activities have more than one effect. An example is fuel used for transport and running of machinery. The financial costs of the purchase of fuel are accounted for and can enter the table as described above. The burning of fuel, however, also has effects on the air and atmosphere. This effect can be identified and described in the appropriate column. There may also be both primary and secondary social and ecological effects of a given activity, and both should be included. For example, the exposure of waste at the tip face in a landfill may attract vermin and create noise (ie. primary effects). The noise and vermin may in turn cause health effects on people working or living nearby (ie. secondary effects). These secondary effects must be recorded.

To address the problem of double counting of costs and benefits, effects have to be divided into single and separable effects, which can then be attributed to specific categories. For example, if the presence of vermin on the landfill affects the health of staff, it will be noted under the category `health and safety'. An effect under the category `Biota' in `Land' will only be noted if there is a separate effect (and so additional cost or benefit) of vermin, such as a reduction in local biodiversity caused by predatory vermin.

For those effects which are not measured through the market and are not already available in dollar terms, further qualification and/or quantification is needed. For example, the quantity and nature of leachate into the ground water will have to be measured.

A variety of assessment approaches were investigated in developing this framework for assessing total cost, many of which are overall approaches for evaluating impacts, effects or costs and not particularly prescriptive of actual methods or tools. An overview of these approaches and tools is provided in appendix 2.

The all-encompassing nature of total cost, as used in this study, means that there are a large range of types of effect to be measured, requiring a variety of tools. Some will require physical scientific measurement, for example air and water quality measurements or measurement of noise levels. Detailed protocols and procedures must ensure that staff carry out field work according to accepted scientific standards. An example is the sampling protocols and procedures of Christchurch landfills (CCC, 1997). Other effects can be measured using social assessment methods (see for example, Taylor et al., 1995) combining a range of information sources (eg., census data, physical impact data and consultative methods). For some effects, it is more appropriate to quantify them using indicators due to their complexity or scale. All of these measurements should be made using robust and reliable methods and tools developed by `experts' in these fields. The focus, however, should not be only on the quantifiable measurements. It may become apparent that some qualitative effects are inappropriate to describe quantitatively (for instance, effects on spiritual values). It is also likely to be inefficient to measure particularly minor effects, or effects which are particularly expensive to measure. Some effects are still impossible to accurately measure, such as the future effects of species loss. Three criteria (box 6) therefore need to be applied in deciding whether and how to measure each effect.

Box 6: Criteria for tools.

1. FEASIBILITY: Are the tools available, reliable and accurate? Is the equipment, time and expertise required realistic?

2. APPROPRIATENESS: Would application of the tools available provide a measure or qualification that reflects the nature of the effect and takes into account social sensitivity?

3. EFFICIENCY: Would the application of the available tools make any significant contribution to our understanding of the total costs, and is the significance worth the cost required to measure this effect?

To measure the magnitude of effects decisions will have to be made on which tool to use. Ideally, effects could be clustered into a few groups with appropriate tools for each of the groups. Section 4.2 discussed the lack of specific tools prescribed within most existing approaches to cost assessment, and highlighted those existing which may be useful (appendix 2). The allocation of tools to types of effect will require further research into the tools available, and possibly the development or adoption of specific tools by appropriate experts.

The approach developed in this report introduces a comprehensive and integrative framework for environmental effects assessment. In most cases, tools are neither specified nor excluded. Instead, the framework provides guidelines for deciding which measurement tools to use and methods of integrating the data obtained. Most existing relevant monitoring procedures can be included in the total cost assessment procedure, unless there are tools available that better meet the three criteria of appropriateness, efficiency and feasibility (box 6). Continued use of present monitoring procedures would maintain the continuity of data, and conserve the resources required to design and implement new monitoring protocols.

The inclusion of the current waste stream analysis commissioned by Christchurch City Council is, however, a significant issue that will require careful consideration. The existing waste stream studies completed every two years for Christchurch City Council provide valuable information for use in waste management decision making. The studies allow the identification of issues relating to waste composition, quantity, and origin. Changes in the behaviour of waste generators between studies may be identified, demonstrating the effectiveness of management techniques, or the need for new techniques. However, waste type was not chosen as a categorisation method for the total cost assessment framework presented in this report, and this renders the data more difficult to include this type of information within the total cost assessment (TCA) framework. Two options have been considered for the utilising waste composition data within the TCA framework.

Some wastes are separated by type for recycling, composting, and treatment, and become different activities in their respective programme, such as soft-drink bottle recycling. The effects of these waste types are therefore easily separable because they are determined by the activity to which they relate. The difficulties arise with programmes which deals with mixed waste, such as landfilling and incineration. An extension of the activities list, artificially creating activities related to the processing of each waste type, would enable the waste composition data to be directly involved in the total cost assessment framework. With reference to the `landfill programme' example, this would involve extending the `existing landfill' activity, presently representing the action of having mixed waste present in the landfill, to contain categories such as plastic, building waste and paper. Effects relating to the presence of a certain waste type in the landfill would then be attributed to the appropriate activity. Determining the effects of a certain waste type would initially rely on research completed elsewhere and may be most efficiently carried out on a national basis. This could include data derived from life-cycle analysis. Life cycle analysis is a complex process requiring high levels of information. The MfE is already involved in life-cycle assessment, and it would not be necessary to commit local resources to this research.

The difficulties with this approach derive from the uncertainty relating to the interactions within a landfill. The complex chemical, biological and physical processes within a landfill make tracking effects to an individual waste type difficult. External conditions such as rainfall, temperature and water table fluctuations also affect the processes within the landfill, making it difficult to directly link causes (presence of waste type) and effects.

Mixed wastes are currently included in the framework by assuming that each unit of waste passing through the same activity has the same composition. The composition is considered to be an average determined by waste composition data. The analysis of waste composition can be used in parallel to the total cost assessment procedure. Management decisions based on the composition of the waste stream could still be made from the waste composition data, as is done at present. Changes in the composition of the waste stream can be compared against changes in the effects of different activities. For example, trends in waste composition and leechate to groundwater in a landfill can be compared and statistically analysed (for example, correlation coefficient) to establish whether there is any significant relationship between them.

The second option for increasing the inclusion of the waste composition data involves retaining the waste stream analysis in parallel to the total cost assessment, but increasing the detail relating to the input. As with the first option, this would involve discovering the effects of each waste type when it passes through an activity. This information would then be used as a basis for adjusting to the "average" cost of a unit of waste, when decisions relating to waste composition are required.

The analysis of these options is not complete, but indicates that waste composition data can be included through the application of information gained through life-cycle analysis. It would be preferred that the effects of each unit of waste delivered to a refuse station could be assessed accurately based on the quantity and composition of the load. However, the direct lines of cause and effect are difficult to determine when waste is mixed and quantities are high, such as in a landfill. It is felt that this issue is one which requires more specialised research, and particular attention. The inclusion of existing monitoring data into the total cost assessment process is therefore considered a priority for future analysis.

In section 3.5 we have discussed the potential of calculating costs in common units, referring both to the issues of feasibility, efficiency and appropriateness. This section reflects the conclusions from that discussion in that we consider it inappropriate, inefficient and infeasible to calculate all effects in the same common unit.

Traditionally, many research projects have relied on one method of data collection and analysis. However, there is realisation "that every researchers, perspectives, methods are value laden, biased, limited as well as illuminated by their frameworks, particular focus and blind spots" (Banister et al., 1994, p.145). Triangulation, that is allowing and making use of a combination of methods, investigators, and perspectives, thus facilitating richer and potentially more valid interpretations, is increasingly used as a methodology for many research projects. It is a small step to suggest that the same is true for the use of different units in measuring costs and benefits. Using an appropriate combination of approaches and tools increases the confidence that it is not some peculiarity of the effects itself or tools used that has produced the findings (ibid., p.146). As Marilyn Waring mentioned, referring to the biased nature of calculating GDP and the need for including other aspects of `production' not necessarily measured in dollar terms, human beings are intelligent enough to compare different units (Waring, 1996, 1998). Willis (1997) states, when discussing the wider use of Full Cost Accounting, that "where practical, external costs (and benefits) are given monetary amounts, otherwise, quantified and /or qualitative information is given" (p. 49). We agree and propose that CCC takes a similar approach.

Several options for units of costs exist (eg., dollars, indices, emergy units, or a combination of these). Financial costs will already be available in dollar terms. As discussed in the previous section, effects not accounted for in the current market and not available in dollar terms will have to be calculated into dollar terms. The criteria provided above (box 6) can guide the user on whether to calculate costs in dollar units. Appendix 2 helps in choosing the appropriate tools for the calculation, ie. how to calculate the effects.

A total cost table summarises the results of each of the steps above. All effects, some with a description of the effect, some quantified and/or with qualitative information, and some in dollar terms, will be compiled in a comprehensive database. This table will be complex, but is needed to ensure total cost assessment and that no effects and their costs and benefits are left out.

For reporting requirements, however, there needs to be a separate structure developed to extract the most important issues and results out of the total cost table. This reporting structure is discussed in the next section.

At this stage in the total cost assessment process, a large amount of data in different forms will have been gathered and compiled into the comprehensive total cost summary table. Monetary values, indices, descriptions and other qualitative and quantitative measures may be present, depending upon decisions made at earlier stages.

The uptake of information by human beings is limited (Griffin, 1994). Presenting the gathered information in a brief, understandable form for decision makers and the public will be a challenge. However, it is a necessary step for fulfilling accountability and transparency criteria (see box 5). Reporting total cost of waste management will have to be flexible and adapted according to the audience (wider public, decision-makers, academics). That is, different levels of detail of information will have to be provided.

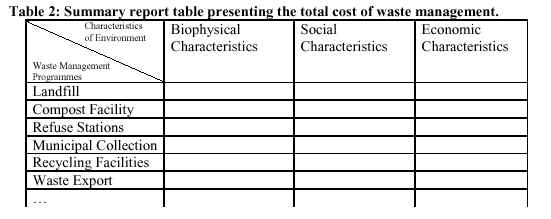

An example of how reporting could be done using a summary report table is provided in table 2. This table would allow data to be comprehended and understood more readily.

The form of a summary table would be similar to the final total cost matrix in that programmes and activities would provide one method of categorisation while the characteristics of the environment would provide the other. However, much broader categories would be used in both methods. For the highest level of summary, a list of programmes would be presented, and the biophysical cost, social cost and economic cost of each would be presented. An example of this format is presented in table 2 .

The information contained in each of the cells would present an approximation of the total cost of the programme. In the "economic" column, a monetary value could be stated. However, in the other columns, non-monetary values will contribute to the total cost. Stating the cost available in monetary values within each cell may be an option, and this would provide for easy comparison between programmes. This method would also allow comparison between charges and total cost, and may be useful in the setting of charges. Unfortunately, this method would not present important non-monetary costs, that in some cases may outweigh the monetary costs of a programme. For example, illegal dumping has almost no economic cost and potentially very high biophysical and social costs. Decisions made using that type of summary report table will not take the non-monetary costs into account, reducing the usefulness of the total cost assessment for measuring environmental performance.

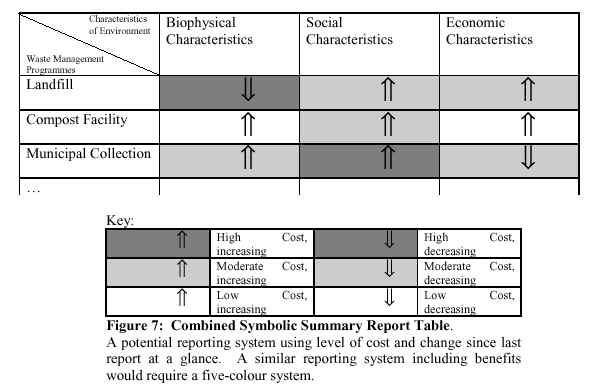

Another possibility is to present a combination of monetary cost together with the non monetary costs, eg., key qualitative descriptions and quantitative measurements (sums) in a summary report table. However, this reduces the understandability and conciseness of the table. To overcome both the limitations of losing non-monetary costs or being too complicated, a single indicator for each cell, or a compound index could be used. The Ministry for the Environment's Environmental Performance Indicators Programme (MfE, 1997c) would be a source of potential indicators, and this would reduce the need for primary research on the part of CCC. However, this would not provide most readers with the information they require, ie. a single value of total cost of the waste management programme. The value in the cell should be accompanied with a target value of high environmental quality, preferably the value of the indicator associated with the absence of the waste management programme (baseline). Table cells filled with actual and targeted values of indicators would then allow comparison of actual and target costs.

To avoid the need for scientific knowledge on the part of the reader, a summary table filled with monetary, indicator and index values would need to be converted into a more readily understood system. The requirement for this system would be satisfied by a combined symbolic system, using colours to represent the magnitude of the cost of a programme, and a set of symbols showing reduction or increase in costs. The colour coding system, known as a "traffic lights" approach to environmental quality reporting, has been suggested for use in presenting sustainability assessments (John Peet pers. comm., 1998). The reduction and increase symbols allow a single table to display the effects of changes in management over time. An example of what this table might look like is presented in figure 7.

As illustrated in figure 7, presentation of the total cost of waste management programmes, and comparison between programmes, is easy using this system. This approach, while not aiding the assessment of setting waste charges, is very useful in environmental performance reporting. The method can be used whenever a quick assessment or comparison needs to be made, at any level of summary. For example, the same table could be used to report environmental performance within a programme, or even between related activities. Another advantage of this table is that particular activities imposing high costs on particular characteristics of the environment can be easily identified. These environmental "danger points" can then be directly addressed by management decisions.

For the application of the total cost assessment process to generator-pays charging, it is anticipated that more conventional reporting techniques would be used. Only monetary values can be directly used to set charges, so established accounting procedures can be used to monetize these values. Using only money values, "appraisal of environmental effects will inevitably omit a great deal from their attempt to value costs and benefits", and therefore affect decision making (Winpenny, 1991, p.72). There is considerable debate over the appropriateness of money-only effects evaluations, even within economics (Portney, 1998; Hausman, 1993).

Within New Zealand, MfE has stated that because it is "virtually impossible to quantify [environmental and community impacts] in terms compatible with economic analysis", they can be treated as intangibles (Young-Couper and McDermott, 1993, p.48). The PCE recommend that "intangible" costs, meaning effects that cannot be easily converted into monetary values, be "explicitly acknowledged" rather than attempting to artificially place monetary values on them (PCE, 1993, p.20). This approach is also applicable to annual reporting. For this reason a protocol on the use of monetary values would be useful, for instance, stating that totals of monetary values should not be presented without simultaneous reporting of important non-monetary costs. Attempts may also be made to offset some of these costs through charging to provide fairly based incentives and disincentives, and to ensure that transparency and accountability criteria are met. All costs potentially contributing to charging must be reported when charging decisions are considered. Finally, the method of deriving charges form the TCA must be communicated to the affected parties.

Summary reporting is the culmination of the total cost assessment process. While the form and the right kind of reporting will rely on the type of information required, enough must be provided for informed decisions to be made, and it must be in a form that is understandable for the intended audience. The options presented here, for charge-related information and for general audiences, allow reporting to meet the criteria used in the creation of the total cost assessment framework (box 5).

The framework described above shows the complexity of TCA. Identification of the costs and benefits of waste management is complex because of the many programmes and activities within waste management, the many effects and their inter-relatedness, the potential use of various units for measurements, and the variety of tools to apply (many of which are resource intensive).

Comprehensive assessment of total cost of waste management will not be achieved immediately and will require a long term and strategic approach. Its full implementation requires time and will have to be done step by step. The total cost framework will therefore have to be regularly evaluated and the performance of TCA continuously improved.

Continuous improvement provides several advantages. Firstly, easier tasks can be completed relatively quickly. For example, the costs of land occupied by waste management facilities, such as refuse stations and landfill sites, can be included in the TCA. Secondly, realistic time frames remove the fear about an over-demanding task, and allow necessary skills for TCA to be developed. For example, the use of non-market valuation tools to assess Christchurch's waste management will only be accurate if its design is sound. Thirdly, the system of TCA can be tested in small parts, for example, for single programmes as a pilot study. The performance of the framework can then be evaluated and further improved. In this way, major financial and social setbacks can be avoided. Lastly, continuous improvement retains flexibility and allows for constant adjustment of how to implement TCA according to new policy developments and requirements. This advantage complements the second framework criteria , which states that the framework must be flexible enough to adjust to new policies (section 4.1).

Continuous improvement acknowledges that not everything can and should be done at once. Only a few effects can be selected for assessment at any one time. However, it is important that the quality of existing assessments is maintained, ie. backsliding is avoided. This means that total cost needs to be continuously checked to evaluate whether cost and benefits already assessed are still accurate (Ostrenga et al., 1992).

Total cost assessment can be used as a tool to evaluate and assess the performance of waste management as a whole, measured against the goals and objectives of the Draft Plan. In particular, TCA allows statements to be made on minimising effects of waste management.

The framework provides a basis for assessing and reporting total cost. As mentioned in section 4.4.5, the framework does not provide a complete set of methods and tools to undertake an assessment of the total cost of waste. Further development of the framework is required. Waste management programmes for Christchurch City have been identified (figure 5), and further hierarchal subdivisions (into activities and sub-activities) will still have to be carried out. This includes all waste management activities which are the responsibility of CCC (including activities of private contractors). Additionally, CCC needs to identify specific tools to measure the effects for a given waste management activity. In order to select tools, these need to be evaluated against a set of criteria. The three criteria identified in this study (feasibility, appropriateness and efficiency) need to be further developed into a general schedule. The schedule can be used to decide how to allocate appropriate tools to measure specific effects.

The following evaluates the potential effectiveness of the developed TCA framework against each of the criteria established in section 4.1.

1. The framework developed for total cost assessment can contribute to Principle 4 of the Draft Plan as well as other principles and aspects of the Draft Plan. Other local, regional and national policy requirements in relation to Christchurch's waste management, particularly the Resource Management Act 1991, and the Local Government Act 1974 and subsequent Amendments are also regarded.

2. The framework is flexible and can adjust to changing waste management practices because the break down of programmes and activities can be changed. Changing social and ecological circumstances are regarded due to the comprehensive identification of the characteristics of the environment. Changes in the application of total cost assessment will be possible in the future. A variety of approaches and tools are part of the framework so that their improvement can be included in the framework. Continuous improvement is considered as important, which further enhances the flexibility. However, other options for a comprehensive framework which are structured differently could emerge. Flexibility to incorporate a completely new option would be problematic.

3. Based on the characteristics of the environment provided, the framework is designed to include all social, biophysical and economic costs and benefits in TCA, thus including `externalities'.

4. The inter-relationship between various effects can be identified by systematically identifying whether and which effect for each activity and each characteristic of the environment exists. This will also enable the identification of primary and secondary effects. For example, the introduction of pollutants to a stream as well as initiatives to mitigate the introduction can be identified as activities.

5. Partly, effects can only be traced back to their causes on a broad level. As discussed in section 4.4.9, the effects on the environment cannot directly be allocated to each waste type if mixed waste is disposed. However, in mixed waste disposal, cause and effect can be linked on a broad scale, ie. if big changes in the waste composition occur over a longer time period, a change in effects will be measurable. Where different types of waste are managed separately, for example, in recycling and composting, the causes and their effects can be linked.

6. The categorisation according to programmes and activities directly reflects the practices in waste management.

7. The systematic approach to TCA provides transparency, accountability and understanding. For example, the costs and benefits of one programme can be regarded separately to other costs and benefits.

8. As discussed in sections 3.5 and 4.5.5, a combination of units for measuring costs and benefits is necessary because it is not always feasible, appropriate and effective to measure effects in a common unit. This impedes the various applications described in section 1.2. However, the TCA framework pursues measuring and calculating total cost as far as possible. Thus, it still provides a valid basis for the applications, including developing a charging structure.

The framework for total cost assessment addresses the established criteria to a very high degree. Consequently, the framework can be useful for a better understanding, and management of total (particularly social and biophysical) cost. However, the framework must be developed further and continously improved.

The framework designed in this study has some features that reduce its performance in some respects. These include taking a reductionist approach, difficulties dealing with special waste types, and restrictions relating to the scope of this study.

The approach taken to total cost assessment in this study is reductionist, meaning that the form of analysis involves reducing a system into components, studying those components, then reassembling the data to study the system as a whole. Reductionist analysis, while the standard for science for the last 300 years, has drawn criticism from some sources that favour an holistic approach, studying the system as a whole. Traditional Maori analysis techniques are holistic, and in some cases, a reductionist approach to total cost assessment may not be able to encompass traditional Maori concerns.

The focus of this study is primarily total cost assessment as opposed to reporting. Reporting has been discussed as it is closely related to assessment, but it is an area which will require further development. Similarly, ongoing evaluation and review will be an important feature of an operational TCA framework, but the incorporation of a monitoring and review system for the framework is not undertaken in this study.

The framework designed in this study can be applied to a range of applications, one of which is charging. Consideration of generator pays issues revealed that charging by waste type would be very difficult to administer effectively on a wide scale (section 3.4). Given this and other considerations discussed, waste type was not selected as a classification system in the TCA framework. Should charging by waste type be pursued, this framework will not provide a direct basis for setting charges.

This chapter developed a framework for total cost assessment to be used for Christchurch City Council's waste management. Firstly, eight criteria for a TCA framework were established. These addressed political requirements, flexibility, the problem of `externalities', the inter-relationship between aspects, the link between cause and effect, waste management practices, transparency, and possible applications of the framework. A discussion of potential approaches and tools currently available such as Environmental Impact Assessment and Non-Market Valuation showed that no one of these fulfil all the criteria. Thus, the need for a new approach, incorporating elements of the existing approaches and tools was apparent. The process of developing this new approach lead to a framework which assessed the total cost of waste management according to waste management practices (ie. waste management programmes and activities) and characteristics of the environment. Subsequently, the nine steps of this framework were described. These identified waste management programmes, the activities and sub-activities of each programme, the characteristics of the environment, and the potential effects of specific activities, measuring the magnitude of effects, calculating effects in units of cost and benefit, compiling the total cost table, reporting the total cost of waste management, and evaluating the framework. The waste management programme `landfill' is used as an example to illustrate how the framework for TCA should be used. The example included the identification of activities within the programme `landfill', a full categorisation of characteristics of the environment, and a guide showing possible effects. Finally, the assessment of the framework against the established criteria revealed that six out of eight criteria are fully met. The two criteria `linking cause and effect', and `working towards a format of generator pays charging without precluding other applications' were partly fulfilled.

[3] There are many cases where identification and measurement of effects cannot be separated. To know whether waste in an existing landfill has effects on the ground water, the ground water/leachate will have to be monitored in order to identify the effect. We have separated the two steps to allow for a comprehensive and logic process to ensure that all potential effects of waste management are identified.

|

|