This page is not a current Christchurch City Council document. Please read our disclaimer.

![]()

|

|

"The consumer society has now become the norm with little thought as to its ultimate consequences" (Boyle in ISWA, 1997, p.44).

In New Zealand, our standard of living is perceived to depend on the use of many products, which, when finally disposed of by the end user, become waste. The New Zealand economy relies on the production and export or import of goods which create `waste' during the production process and which become waste when discarded at the end of their lifetime.

The image of New Zealand as a `clean and green' nation has been questioned internationally (B�hrs & Bartlett, 1993). As noted in the State of New Zealand's Environment Report "the small size of the New Zealand population and the relatively large land area and water resources at our disposal have allowed us to have our environmental cake and eat it too" (MfE, 1997). For many years New Zealand has neglected the effects and associated costs of waste and its management (PCE, 1998).

As awareness of waste management issues has risen, policy makers have given thought to the `ultimate consequences' of a `consumer society' for the people and environment of New Zealand/Aotearoa. This is reflected in central, regional and local government policy and is encapsulated in Principle 4 of the Christchurch City Council (CCC) Draft Waste Management Plan for Solid and Hazardous Waste (CCC, 1998), which states that:

The real costs of waste management shall include social, environmental and economic costs and these will be assessed and reported annually.

In this report we address this issue and make recommendations on how CCC should assess the total cost of waste management in Christchurch City.

This report has been completed for the Waste Management Unit of the Christchurch City Council. The authors of the report are five Master of Science students studying in the Resource Management programme, Environmental Management and Design Division, Lincoln University. More detailed information on the authors is provided in Appendix 1.

The aim of this report is to provide a framework for the assessment of the total cost of waste management in Christchurch

Five objectives have been established for this study. These were derived from the terms of reference set by staff from the Environmental Management and Design Division in collaboration with the Christchurch City Council Waste Management Unit.

All of the objectives are addressed within this report. However, the research group's interpretation of and approach to addressing the objectives altered through the course of the research programme. These changes reflect the nature of the research process and exploratory nature of the topic and represent a rational, logical and intuitive progression as the research group's `body of knowledge' increased. The objectives and the degree and nature of alterations are listed and discussed below.

Objective 1 was initially considered to encompass understanding general waste management concepts and issues as well as the specific operational environment and issues for Christchurch City. The research group recognised the need to examine issues which were not directly related to waste management practices or issues but which had a potential bearing on or implications for total cost assessment of waste in Christchurch City (eg., the importance of past and future costs, the generator-pays principle and tangata whenua issues).

`Components' have been consistently interpreted as any category or smaller unit of cost or benefit which contributes to the composition of `total cost' (as a whole). Objective 2 was initially interpreted as requiring the group to identify `categories of cost' (eg., costs associated with risk, occupational safety and health, and administration) as well as specific costs associated with waste management activities (eg., costs associated with transportation of waste). An alteration in the research approach has been to give greater emphasis to the identification and analysis of `categories of cost' (eg., effects-, programme-, and waste type- based categories) as opposed to providing a comprehensive account of specific costs and benefits for waste management in Christchurch City.

The rationale for this emphasis is that a series of important steps precede the comprehensive identification of specific costs and benefits. Firstly, it is necessary to examine issues which affect total cost assessment in order to ascertain implications for development of the framework. Secondly, a systematic and long-term approach to the assessment of costs and benefits is required. Thirdly, comprehensive identification requires a detailed understanding of waste management programmes, activities and dynamics before specific costs and benefits can be identified.

Each of these steps requires considerable research, and the group have been strategic in terms of the order and number of steps taken. Steps taken in the course of this study are outlined in section 1.1.3.

Objective 3 was initially interpreted as requiring assessment of barriers to TCA. These include ethical (is it appropriate?), technical (is it feasible?) and resource barriers (is it efficient?). Related to this is the need to identify potential approaches or tools for assessing cost, and to assess their benefits, limitations and potential application. The research group's approach has been to give greater emphasis to evaluation of potential tools or approaches other than TCA.

Objective 4 has been consistently interpreted through the course of this study. The feasibility and appropriateness of measuring costs in common units (in general and specifically for money) needs to be determined (Is it feasible to convert costs into a common unit? Is it ethical to convert costs into a common unit?). In addition, the potential for use of Net Present Values and discount rates for the assessment of total cost should be discussed to fulfil this objective.

This objective has been consistently interpreted through the report. An approach to implementing total cost assessment should be developed and illustrated using practical examples. The intended output of this research project has changed slightly in accordance with alterations described above, as follows:

Rather than preparing an inventory of specific effects and associated costs for waste management programmes and activities, a systematic approach to implementing total cost assessment will be presented. This will be discussed in the context of issues which effect total cost assessment of waste in Christchurch City. The research output will include practical examples of framework application, and options and recommendations which outline a clear course of action for the CCC Waste Management Unit.

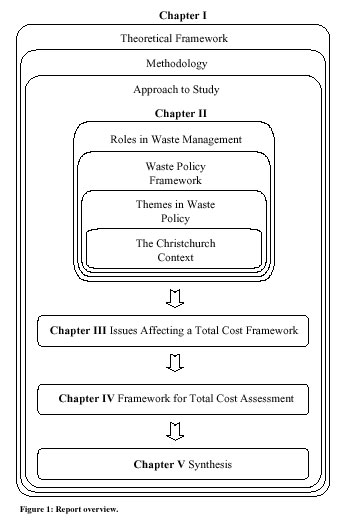

A broad overview of the report structure is presented in figure 1. This figure illustrates the overarching influence of the theoretical framework (the research group's underlying theories) which shapes other parts of the report, and from which the study methodology and approach are derived (Chapter 1).

Chapter 2 of the report examines the process of waste management in Christchurch City in a broader waste management context. Roles of organisations in waste management are discussed and policy influences on CCC are described. Key themes and trends within the policy process, and specific features of Christchurch City's waste management system are discussed. Chapter 2 closes with a discussion of important terms used.

Issues which affect a framework for total cost assessment are discussed in Chapter 3 of the report. These include the nature of effects, tangata whenua, differences between public and private delivery of waste management services, the generator pays principle, measurement of effects in common units, import and export of waste, coordination between organisations, and issues relating to future costs and benefits.

Chapter 4 of the report presents and evaluates a framework for total cost assessment. The reasons for developing a framework are discussed and criteria for evaluating a TCA framework are specified and justified. Other approaches to total cost assessment are discussed and their benefits and limitations described. The broad approach to framework development used in this study is then discussed.

Nine steps for implementing the TCA framework are described and illustrated using `landfill' as an example. The potential use of monitoring (including indicators) and the principle of continuous improvement are then discussed. The TCA framework is finally evaluated against the criteria specified.

Chapter 5 reviews and summarises earlier Parts of the report and draws options, conclusions and recommendations. This includes a review of options and decisions made in the process of developing the framework. Four options are then described and evaluated (in relation to specified criteria) to determine whether TCA should be implemented. Conclusions from the report are drawn and recommendations are subsequently given which advise CCC on how to implement the TCA framework. The report finishes by identifying five prioritised steps toward implementation of the framework.

The information obtained by TCA can be applied in various ways. A framework for total cost assessment needs to take account for the intended applications. The following main applications are possible.

1) Annual reporting: The hierarchical and systematic structure of a total cost assessment by using a framework contributes to transparent, accountable and understandable presentation of total cost and its use in planning. TCA can therefore be used for annual reporting. Principle Four of the Draft Waste Management Plan for Solid and Hazardous Waste states annual reporting as a direct application of TCA (CCC, 1998).

2) Education and promotion campaigns: Information on total cost can be used for education and promotion campaigns, and consultation process to address the goals of minimising waste and its effects on the environment. Therefore, TCA can facilitate the Draft Plan's sixth principle of education and consultation (CCC, 1998).

3) Best management practices: A systematic break down of costs and benefits allows CCC to target the improvement of specific programmes or activities within their waste management services to minimise waste and its effects.

4) Implementation needs of the RMA: Total cost assessment addresses the effects of waste management activities on the environment. The framework therefore has potential uses under the RMA. For example, TCA can be useful to fulfil the duty to assess costs and benefits (s32) and effects on the environment in relation to a resource consent (s88(6)(b)), and to assist councils in the efficient use of natural and physical resources (eg., landfill space) (s7).

5) Charging: Using the information provided by total cost assessment, generators of waste and users of waste management services can be charged on the basis of the total cost in accordance with the generators pay principle (section 3.4). It is CCC's primary focus (E. Park, pers.comm., 1998) to use TCA for developing a system for charging which is based on total cost.

This study takes a wide approach in that the framework for total cost assessment is developed in a way so that TCA can be potentially used for all applications. However, dependent on the actual applications, the framework can be developed further in specific directions.

The purpose of this section is to make explicit the otherwise unseen theories which underpin both the problem this study group was presented with, and our approach to it. It locates waste management in context as one phenomena within the environmental `problematique' (widespread, inter-related, complex environmental problems), which requires an integrated approach. This approach requires careful consideration of a broad range of policy, ecological, social and economic issues which surround our key `problem'. While these influences and issues are dealt with in the body of the report, there is a particular theory which is influential both in waste management policy and in the concept of total cost of waste management itself, which is often not made explicit: neoclassical economic theory. We also recognise total cost as a product of an international trend of more integrated assessment of the effects of human activity.

Awareness of environmental issues began to increase in the 1970s (B�hrs and Bartlett, 1993). In the decades that followed, there was a "growing realisation... that policies addressing only one medium (air, land or water) at a time and only `at the end of the pipe' rather than at the source or ultimate destination, were not fully successful and in some cases were compounding the problem" (Bartlett, 1990, p.236). Increasingly, environmental `problems' are recognised as complex and interrelated, and waste management is no exception (B�hrs and Bartlett, 1993).

"One of the key reasons why environmental policies have not been very successful is that often they recognise only inadequately or not at all the complexity and interrelatedness of the phenomena that constitute the environmental problematique". (ibid, p.9)

The term `environmental' is potentially all-encompassing - it includes the physical or natural environment, and also human communities (section 2.5). Solid waste management, as an `environmental' issue, likewise contains social, political, institutional, biophysical and economic facets. Beyond that, it is also inseparable from wider environmental issues like resource consumption patterns. In response to this complexity, and frustration over the inadequacy of fragmented, reactionary responses (ibid), arose Integrated Environmental Management (IEM). IEM is an approach to environmental and natural resources planning and management which is:

These characteristics translate into a process for addressing environmental problems. Comprehensiveness means starting with a wide initial scope to identify all relevant factors (social, cultural, economic, political, institutional, biophysical). Interconnective means addressing the inter-relationships of these aspects through systems analysis and information management systems like GIS (Geographical Information Systems) and databases. Despite a large amount of interconnected information, "it should be possible to obtain the benefits of a comprehensive outlook without becoming so entangled with a complex web of interrelationships that that management exercise literally disappears into a `black hole', never to re-emerge", by taking a strategic approach (Mitchell, 1987; cited in Born and Sonzogni, 1995, p.171). To be strategic means "to pragmatically scale down the effort", and refers to reducing the scope to key issues and pressure points through analysis and trade-offs between options (Born and Sonzogni, 1995, p.171). The final phase of IEM is being interconnective, which means involving and coordinating the parties and institutions affected by or affecting the `problem'. What is being integrated by IEM is different components of the physical or biophysical environment (eg., land, air, water, biota), interpretations of them (eg., economic, socio-cultural and biophysical), and the policies and institutions surrounding them (B�hrs, 1995).

The aim of this report is to provide a framework for the assessment of total costs of waste management in Christchurch. This responds directly to Principle Four of the Draft Waste Management Plan for Solid and Hazardous Waste (the Draft Plan), that the "real costs of waste management shall include social, environmental and economic costs and these will be assessed and reported annually" (CCC, 1998). This plan was developed to meet the requirements of the Local Government Amendment Act No. 4, 1996, which placed a new emphasis on funding, the use of economic incentives and disincentives to meet aims, and having "regard to environmental and economic costs and benefits for the district".

These changes are in keeping with a trend in the state sector's approach since 1984, when government interventionism and activism were rejected in favour of a market driven approach expressed through financial deregulation, liberalisation of markets and trade, restructuring of the state sector (including local government) and a new emphasis on fiscal restraint in government activities (Kelsey, 1995). The change this marked was hugely significant - "apart from the changeover from Maori to British government in the 1840s, no period has seen such policy change" (James, 1993, p.10). The desire to reduce general spending and the application of corporate structures to the state sector has seen transparency and financial accountability become increasingly important values. Public participation was also a feature of both the new institutions developed (such as the Resource Management Act 1991), and of the reforms themselves (Memon, 1993, p.96). These key ideologies are clearly expressed in the Draft Plan.

Central to the approach adopted by the New Zealand Government in 1984 was Chicago School economic and public theories (Jesson, 1989, p.67; Easton, 1989, p.121), "implemented in almost undiluted form" (Kelsey, 1995, p.55). The Chicago School combined economic theory with libertarianism to endorse a laissez faire approach which reduces state controls and increases reliance on market-based tools (Jesson, 1988; Smith, 1988). This influence has extended directly into the government's environmental management policies and waste management itself, as shown by the Ministry for the Environment's Landfill Full Costing Guideline (MfE, 1996a) which opens its background section with the statement: "The theory of resource economics says that environmental damage occurs because prices do not reflect the true cost of resource use". Central Government policy directly prescribes generator charges for waste management as part of an overall policy to internalise externalities wherever possible (Environment 2010 Strategy - MfE, 1995, pp.15, 45). This economic background is clearly significant to the concept of total cost in waste management, but is not always explicit in its policy, such as the CCC's Draft Plan. It is therefore important to outline neoclassical theory and its expression in resource economics, as relevant to total cost in waste management.

Neoclassical theory's roots are in the classical economics of the 1700s (characterised by Adam Smith's `invisible hand' and Malthus' and Ricardo's resource scarcity theories). In this era the notion was developed that rational individuals acting in a self-interested fashion could collectively serve social interests. Long term physical constraints on growth were modelled by Malthus and Ricardo. In the late 1800s neoclassical theory developed, and the scarcity of resources facing infinite wants became central. From this focus comes the concepts of supply and demand and increasing emphasis on marginal analysis (ie. considering the trade-offs made by producers and consumers as they respond to this scarcity according to their preferences). Interaction between supply and demand results in a market equilibrium (at the point where marginal benefits equal marginal costs). The market equilibrium is socially optimum in that nobody can be made better off without making somebody else worse off (ibid.). This state is called Pareto optimality, and that it is the socially optimum state is the first law of welfare economics (Feldman, 1980).

The rational egotistic individual or `economic person' is a key assumption, and the perfect market model in which equilibrium is reached includes the following further assumptions:

1. information is freely available to all actors in the market;

2. property rights are fully defined;

3. competition is complete: there are many buyers and sellers, and free entry and exit from industries; and

4. there are no transaction costs.

The absence of any of these conditions is known as market failure. In reality of course, perfect market conditions never exist, but market failure is particularly associated with natural resources because biophysical goods (eg., clean air) and services (eg., assimilative capacity) frequently have ill-defined property rights. The result is that responsibility is not taken for actions (such as pollution of public goods like air and water), by the user. This creates a divergence between social costs and private costs, as the levels of resource or biophysical capacity use chosen by the user does not include all the costs of their action. The unaccounted for costs (`externalities') are borne by society as a whole.

If these externalities can be internalised, the market will still be capable delivering correct allocations of resources, levels of pollution and so on (Pearce and Turner, 1990, p.64). This has resulted in a great popularity of `economic instruments' for resolving environmental problems. However, Pareto optimality is not necessarily compatible with other policy goals such as equity. This relates to the second law of welfare economics, that Pareto optimal outcome will only be as fair as the initial distribution of resources (Feldman, 1980). Neoclassical theory has by no means gone uncritiqued and there are several branches of economics (eg., see Peet, 1992), as well as other disciplines, dealing with these issues. However, the reliance of overarching government policies in New Zealand on neoclassical theory seems to imply that market solutions to allocative issues are better than the solutions which could be reached by other means, despite the fact that markets will never be perfect.

The persistence of environmentalism, in combination with the desire for accountability (related in part to neoclassical economic theory), has seen a raft of approaches to assessment of the impacts, effects and costs of human activities, looking wider than traditional financial considerations. These include institutionalised requirements for Social Impact Assessment (SIA) and Environmental Impact Assessment (EIA) and, in New Zealand, Assessment of Environmental Effects (AEE) under the Resource Management Act 1991 (see appendix 8). Initiatives have also developed in the private sector such as Total Cost Management and Life Cycle Assessment. Full Cost and Environmental Accounting have developed in response to the lack of accountability (particularly social and biophysical) within traditional accounting systems. These are summarised and discussed in appendix 2, and it is important to note at this point that they contributed to our conceptualisation of total cost.

The concept of `total cost' of waste management, used by Christchurch City Council and this study is therefore a product of economic theory and related policy influences, and of an international trend toward more all-encompassing impact, effect and cost assessment. These and further contextual issues are identified and responded to using Integrated Environmental Management or IEM.

This study focuses on the development of a systematic and comprehensive framework for total cost assessment of waste management, rather than on measuring component parts of total cost. A justification for this approach is given in section 4.3. The research project specifically applies to waste management needs in Christchurch City. The framework for total cost assessment is developed to address issues in a Christchurch-specific context as well as universal issues. Therefore, the methodological approach of in this study is qualitative and applied.

Waste management has biophysical, social, and economic effects. The complexity and interrelatedness of these effects requires an interdisciplinary and integrated approach to total cost assessment. No single discipline can provide the whole answer to how a framework should be developed for total cost assessment. Therefore, theories and concepts from a variety of disciplines have been included and combined in the development of this framework.

The assessment of total cost of waste management, including biophysical, social, and economic effects, is a field which has not yet been researched extensively. There is no widely available theory or application of a theory which addresses total cost assessment as it is defined in this study. Theories and concept must be transferred from several other sources and further developed. Our research can therefore also be described as a combination of descriptive and exploratory research.

This study was conducted in 1998 (February until June). Appendix 2 shows our research process during this period. It shows the steps of our study from the interpretation of the terms of reference to the conduct of our research, analysing the nature of total cost assessment and compiling the final report.

The methods used in our study included document analysis, evaluating the literature. Criteria for evaluation were whether concepts and theories were applicable to total cost assessment. Policies were analysed and relevant policy processes and implications established. We also used interviews to gain knowledge from experts in waste management and total cost assessment. These interviews were semi-structured and open ended, mainly because we wanted to explore their thoughts, and did not want to narrow down the discussion. To further our knowledge and insight into waste management practices we also included visits to transfer stations as an experience.

The need to explore new ways of thinking is expressed in our emphasis on group process. Group discussions are an excellent way of generating and checking ideas, and applying concepts and theories to the study (Brilhart, 1992). Compared to individual research, group work offered advantages for the multi- and interdisciplinary approach. Investigations are a team based process, in which the setting of goals, decision making and time management remain a collective responsibility. Discussion of all major issues by the group and applying different minds throughout the research process resulted in a wider range of references consulted, a more critical debate of the findings and overall a greater awareness of the topic than would have been possible by individual researchers. The different personal background, subject expertise and experience of each group member further helped an interdisciplinary approach.

The particular focus of this study is on assessing the total cost of solid and hazardous waste management. The physical boundaries of this study are the Christchurch City limits, although the foreseeable joint management of a new landfill within the Canterbury Region and its implications on regional waste management are taken into account. The study focuses on post-production waste. This excludes the costs of waste production and minimisation programmes born by the private sector (eg., Cleaner Production), but includes the costs to the Christchurch community of waste collection (both private and public) as well as the costs of the various strategies to reduce, reuse, recycle, and treat the waste until its final disposal. In our study we consider previous, current and future costs of waste management. For a more detailed discussion of the definitions and meanings of the terms used above see also section 2.5.

In dealing with predominantly Christchurch's waste management we focused on Western perspectives and viewpoints. Non-western perspectives could lead to other conclusions, however they are not included.

The group's findings and recommendations, although extensively researched, are focused on the Christchurch area and Canterbury Region. This may limit its transferability to other regions. We provide a framework for a possible way of assessing total costs of waste management in Christchurch, with an example (table 1). It is, however, beyond our resources to provide a complete set of methods and tools to undertake an assessment of the total cost of waste. Further development of this framework will have to be done. While developing the framework, we have taken every precaution to consider potential changes in waste management practices in the near future. The framework is flexible to many changes however, as we cannot foresee all future requirements, some adjustments will have to be undertaken in the future.

Our study is based on the assumption that the institutional frameworks are a given. Although change can sometimes happen overnight, the legal, political, and economic frameworks of New Zealand are taken as a given. This especially is true for the global marketplace and the emphasis on the generator pays concept.

|